Post-2015 Consensus: IFF Assessment, Cobham

Assessment Paper

The initial formulation of a target to address illicit financial flows as part of the Post-2015 Development Agenda was by means of a monetary sum, but the Open Working Group’s current proposals now highlight the importance of identifying specific steps necessary for progress. In this light, we propose and examine three clear, cost-effective targets which could provide the practical framework to support a broad, high-level target.

Alhough this paper provides a tentative economic analysis of the measures proposed, the limitations of benefit-cost analysis should be kept in mind throughout. The power of the original MDGs lies in their setting of norms rather than specific targets and the ongoing process is fundamentally political, with economic assessment clearly taking second place. Nevertheless, benefit-cost analysis still has a role in creating a framework.

Summary of the most high-yielding targets from the paper

| IFF Targets | Benefit for Every Dollar Spent |

|---|---|

| Reduce to zero the legal persons and arrangements for which beneficial ownership info is not publicly available. | $49 |

| Reduce to zero the cross-border trade and investment relationships between jurisdictions for which there is no bilateral automatic exchange of tax information. | Likely to be high |

| Reduce to zero the number of multinational businesses that do not report publicly on a country-by-country basis. | Likely to be high |

Summary

Within the areas identified as political priorities, and alongside the rights-based and other arguments for specific emphases and inclusions, the results of economic cost-benefit analysis can provide additional and complementary evidence. Since a narrow economic approach provides conservative estimates because of the difficulty of capturing wider political, social and environmental benefits, there is unlikely to be a conflict between cost-benefit analysis and rights-based arguments.

Illicit financial flows comprise tax evasion, the theft of state assets, the laundering of the proceeds of crime, and a range of market and regulatory abuses under cover of anonymity. The leading estimates suggest that developing countries in total may currently be losing close to a trillion dollars a year. The hidden nature of the problem makes estimates uncertain, but it seems likely that illicit outflows are substantially larger than official aid receipts and that tax abuse is the major element.

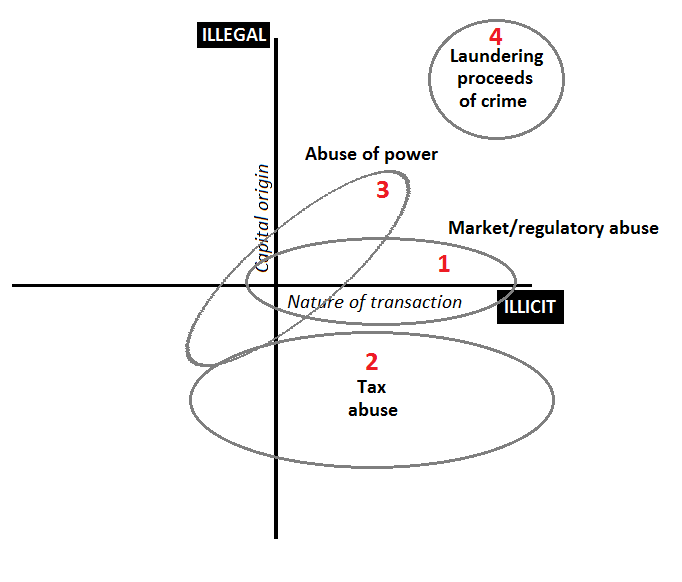

‘Illicit’ flows are not necessarily illegal, since laws vary between territories. Additionally, behavior of uncertain legality is more likely to go unchallenged by a tax system with little to no capacity to uncover corporate tax evasion, or a political system with little to no will to address the theft of state funds. Nevertheless, IFF is by its nature hidden, whether it is illegal or simply unacceptable to the public.

IFF can fit into one of four categories as shown in the figure. This makes clear that the source of funds may be perfectly legal, while the avoidance of tax, for example, may be technically legal but illicit according to societal norms. The historic emphasis in policy has been on IFF relating to illegal capital (abuse of power and corruption, and laundering of criminal proceeds), but measures against tax and market abuse have more recently been given greater prominence.

IFF can fit into one of four categories as shown in the figure. This makes clear that the source of funds may be perfectly legal, while the avoidance of tax, for example, may be technically legal but illicit according to societal norms. The historic emphasis in policy has been on IFF relating to illegal capital (abuse of power and corruption, and laundering of criminal proceeds), but measures against tax and market abuse have more recently been given greater prominence.

Specific illicit flows can generally pass through one of several channels, so a broad approach is needed. The key feature of IFF is their hidden nature and the countermeasures developed take the form primarily of requirements for greater financial transparency: transparency of and about companies, and between jurisdictions in relation to each other’s residents.

IFF in the post-2015 agenda

The original Millennium Development Goals reflected primarily a donor agenda and also focused heavily on the social sector rather than addressing wider macroeconomic issues. The inclusion of a proposed target for reduction of illicit flows reflects the development of a consensus on its importance in recent years. The specific, monetary-based targets for reduced IFF, reduced tax evasion and increased stolen asset recovery are flawed, but should be seen as an important first step in the development of workable alternatives.

Even if reliable estimates of amounts involved could be agreed, the targets focus on financial impacts rather than broader issues of governance and societal impact. The other problem is lack of clear accountability; IFF are an international problem, the secrecy provided in other jurisdictions is at least as important as the action taken domestically.

The Open Working Group on Sustainable Development Goals has in fact developed more detailed goals which emphasize global cooperation and allow better identification of individual issues. A change of metric from dollars to proportionate reduction also places less emphasis on financial impacts. In this paper we develop a proposal for precise targets within the final post-2015 framework.

Development impacts of IFF

Illicit financial flows may have impacts in four important areas: economic growth, social development outcomes, inequality and governance and institutional strength.

The link is most direct in relation to economic growth, where illicit outflows can be considered as lost GDP. For example, a study covering the period from 1980 to 2009 showed 20 Sub-Saharan African countries to have lost more than 10% of their GDP to IFF, with Djibouti and the Republic of Congo losing more than a quarter. The revenue impact (via trade mispricing) for all developing countries was reported to be $160bn in a 2008 Christian Aid report, while a 2010 GFI study estimated a loss of 3.4% of total government revenues in sub-Saharan Africa. For individual countries, the loss is much higher, with Zimbabwe top of the list at 31.5%. All this represents a lost opportunity to develop infrastructure and invest in human capital.

IFF also tend to increase inequality, since it is the elite who have both the most to gain and the access to foreign bank accounts or international businesses. This in itself accentuates inequality because governments are less able to provide health or education benefits or make cash transfers to poor families. It is made worse by governments being forced to raise revenues via regressive indirect taxes such as VAT. There is also a political dimension: as elites battle for control of limited resources, opportunities further down the social scale are further reduced. As well as the direct damage (e.g. to children’s opportunities), greater inequality has been shown to result in a substantial loss of economic growth.

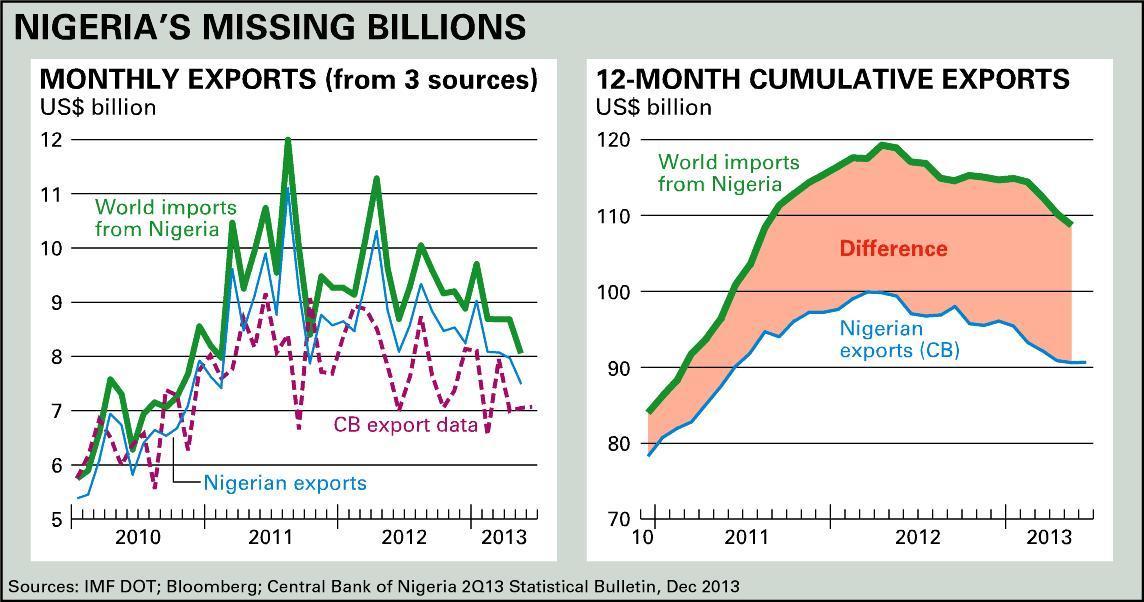

A striking illustration of elite gains was highlighted by the recently suspended governor of the Nigerian central bank, Lamido Sanusi.  The gap between the country’s recorded oil exports (as declared to the central bank in relation to payments to the state oil company) contrast with the apparent worldwide level of imports from Nigeria, as shown in the figure. At the same time, between 1990 and 2010, the vast majority of Nigerians saw their consumption fall, in contrast to large increases above the 95% percentile of income – and in contrast to the pattern in other countries across the region.

The gap between the country’s recorded oil exports (as declared to the central bank in relation to payments to the state oil company) contrast with the apparent worldwide level of imports from Nigeria, as shown in the figure. At the same time, between 1990 and 2010, the vast majority of Nigerians saw their consumption fall, in contrast to large increases above the 95% percentile of income – and in contrast to the pattern in other countries across the region.

The social impacts of IFF have had little attention from academics. However, a 2014 study looked at the effect on child mortality and, in particular, how much quicker towards the MDG (number 4) progress on the issue would have been if IFF had been eliminated. In Swaziland, there was a projected reduction from 155 to 27 years and in Mauritania from 198 to 19 years. The overall picture for Africa shows the projected date for achieving MDG4 moving from 2019 to 2016.

Coming to the final major area of impact, there are multiple channels through which IFFs present a threat to governance, undermining both political institutions and the confidence in them. Abuse of power will obviously have a large direct effect, but the effect of tax abuse may be just as powerful. Although there is a complex relationship between taxation and governance, states with a ratio of tax to GDP below 15-20% are regarded as ‘fragile’ and have insufficient capacity to deliver services without appropriating natural resource wealth or becoming dependent on long-term aid. On average, a 10% improvement in a broad governance measure would imply an increase in per capita GDP of 1.5%, or (allowing for dynamic effects) as much as a 6.1% increase.

Proposed targets

Financial transparency initiatives focus on three areas: beneficial ownership information, automatic exchange of tax information and country-by-country reporting for multinational enterprises, each of which can give a target with clear lines of accountability.

In the case of beneficial ownership, the legal title to companies is not always the same as the name of people who actually control it, and anonymous ownership of companies, trusts and foundations is often the central element of secrecy in illicit flows. The difficulties of ensuring transparency are compounded by the use of foreign jurisdictions, such as Luxembourg or Mauritius. The Financial Action Task Force recommends that the names of the real owners of companies, trusts and foundations are available to the authorities in an adequate, accurate and timely manner. The UK and a number of its territories have committed to a public registry of beneficial ownership. Public disclosure allows citizens as well as the authorities to hold companies to account.

Since a partial solution to the transparency issue would simply allow alternative jurisdictions to continue to be used, a zero target is necessary:

i. Reduce to zero the legal persons and arrangements for which beneficial ownership information is not publicly available.

The second target relates to multilateral, automatic exchange of tax information, which would provide a powerful deterrent to undeclared foreign income and hidden assets as well as tackling continuing abuse. The G8 and G20 have made declarations in favor and the OECD’s latest Common Reporting Standard contains important transparency requirements. An ‘early adopters’ group has now begun the process to pilot the standard. Encouragingly, this involves a number of traditional ‘tax haven’ jurisdictions, such as Jersey, Cayman and the British Virgin Islands, but few developing countries and not even all the G20 members. The target for this issue is:

ii. Reduce to zero the cross-border trade and investment relationships between jurisdictions for which there is no bilateral automatic exchange of tax information

The potential scale of corporate tax abuse in IFF is large and the third target is on corporate reporting. Following a period of growing unilateral public reporting requirements, the OECD has been mandated to produce a global standard which would allow a simple system of red-flagging misalignments of profit and economic activity; if, for example, local subsidiaries account for half of the economic activity but only 5% of the declared profit, while a subsidiary in Luxembourg, for example, is in the opposite position. The reporting envisaged is to the tax authorities, but making the information public would give even greater accountability. The third target is:

iii. Reduce to zero the number of multinational businesses that do not report publicly on a country-by-country basis.

These three measures, between them, point the way towards a set of post-2015 targets that have the potential to generate the type of illicit flow reductions that the High Level Panel proposal envisages. The other potential area target area is mis-invoicing, which can support a broad range of IFF. However, closing one channel merely directs more illicit flows through the remaining ones, so we prefer to take a broad approach to reducing the benefits of IFF via the three targets identified.

Costs and benefits

On the question of beneficial ownership, we consider only companies, since there is too little data available on trusts and foundations. Nevertheless, transparency is equally important for these entities.

A 2007 study of the EU looked at two models: one where intermediaries such as accountants and banks would be responsible for obtaining and disclosing information on ownership above a 25% threshold (model 0) and the other in which any beneficial owner had a duty to disclose any stake of 10% or more to the company in question, who in turn would file it on a Central National Registry (model 1). For model 0, the net direct and indirect costs across the EU amount to €6.7bn and €10.1bn respectively, with the bulk of the costs associated with intermediaries. For model 1, the respective costs are €125 million and €11.2bn, with costs being greatest for government. The bulk of these costs would accrue in the UK: 61.1% under model 0 but 97.6% under model 1. The greatest costs are attributable to loss of tax revenue and loss of bank clientele. On the other hand, aggregate benefits would accrue to more than half the EU Member States.

The NGO Global Witness commissioned a UK study in 2013 which concluded that a disclosure system would cost at minimum £14.08 million for companies to maintain internal registries and approximately double that for the information to be made public. The cost of companies also providing ID verification for each owner would amount to an additional £50 million. Ongoing costs amount to up to £6.5 million annually. Pulling out the UK figures for model 1 from the earlier EU study and the closest scenario from the UK report and converting both to 2013 dollars gives figures which are nearly equivalent.

However, the UK government’s own 2013 impact assessment estimates a cost to business of £226 initially and £78 million annually thereafter, a total cost over ten years of £899 million (at a 3.5% discount rate), equivalent to $1.4bn. This much higher figure may be due in part to self-reported costs from businesses, but we take this figure as the basis of our high cost scenario. The UK government’s ‘low’ estimates are used for our medium cost scenario, while the figures for our low cost scenario come from the Global Witness study. Our extrapolations to a global level assume either a UK level of costs throughout, or a lower level which takes account of the variation across the EU. We also consider three benefit scenarios: a baseline of 2011 illicit flows with an assumed 50% reduction, and the average illicit flow for 2002-11 and either a 25% or 10% reduction.

This results, of course, in a very wide range of benefit-cost ratios. For the high benefit/low cost scenario assuming the lower level of global costs, this is over 20,000, but even for the high cost, low benefit case with an assumed UK level of costs, it is a very respectable 13.3.

On the question of automatic tax information exchange, 44 countries and jurisdictions are now piloting the OECD standard, based on the US Foreign Account Tax Compliance Act. Including other jurisdictions committing to the same standard but not part of the pilot, those responsible for more than 90% of cross-border financial service provision are now signed up. Although this is very encouraging, there still needs to be a zero target for bilateral trade and investment without automatic information exchange to ensure that the problem is not simply transferred to the countries not yet included – and that developing countries are fully included in multilateral exchange.

Compliance cost estimates currently remain private, but we have to assume are lower than the benefits. As for benefits, the most recent US IRS study shows a misreporting percentage of 56% for incomes subject to little or no information reporting. This falls to 8% when substantial reporting is required (and there is no withholding). It seems reasonable to assume that the availability of matching information would cut misreporting to a seventh of its level if applied globally. Using the most conservative academic estimate of $4.5 trillion in unreported funds, and assuming them to be invested in US Treasury bills yielding 3.5%, this level of compliance would bring in a further $135 billion of taxable income annually. For a low-end estimate, we can assume tax authorities only reduce misreporting by one seventh, yielding $22.5bn in extra taxable income annually. Over the post-2015 period, these low- and high-end scenarios would yield additional taxable income globally of $245bn to $1471bn at a 5% discount rate.

On the final target of country-by-country reporting by multinationals, there seems to be a positive case, since the OECD is working towards a template to be used by all tax authorities. Publication of the information will increase accountability. To make the process as simple as possible, companies would simply publish the information and record this in an online, machine-readable register. A recent PwC poll showed 59% of business leaders in favor, implying that compliance costs are not an obstacle. Although more work is needed on this issue, tax avoidance appears to be substantial and country-by-country reporting is likely to reduce the most egregious misalignment. A 2% reduction could add $4bn annually to US revenues alone or $56-64bn by 2030.

Conclusions

1. There are potentially powerful post-2015 targets which could ensure the framework delivers major progress in reducing illicit financial flows; all three proposals have high benefit-cost ratios in any reasonable scenario.

2. There is scope to improve significantly the evidence base over the next two years as initiatives in each area go forward.